Nature Reviews: The physics of financial networks

ISC associates Guido Caldarelli and Gulio Cimini coauthored an interesting review on modelling the financial systems and networks now published in Nature Reviews, M. Bardoscia, P. Barucca, S. Battiston, F. Caccioli, G. Cimini, D. Galaschelli, F. Saracco, T. Squartini, and G. Caldarelli. Nat. Rev. Phys. June (2021).

As the total value of the global financial market outgrew the value of the real economy, financial institutions created a global web of interactions that embodies systemic risks. Understanding these networks requires new theoretical approaches and new tools for quantitative analysis. Statistical physics contributed significantly to this challenge by developing new metrics and models for the study of financial network structure, dynamics, and stability and instability. In this Review, we introduce network representations originating from different financial relationships, including direct interactions such as loans, similarities such as co-ownership and higher-order relations such as contracts involving several parties (for example, credit default swaps) or multilayer connections (possibly extending to the real economy). We then review models of financial contagion capturing the diffusion and impact of shocks across each of these systems. We also discuss different notions of ‘equilibrium’ in economics and statistical physics, and how they lead to maximum entropy ensembles of graphs, providing tools for financial network inference and the identification of early-warning signals of system-wide instabilities.

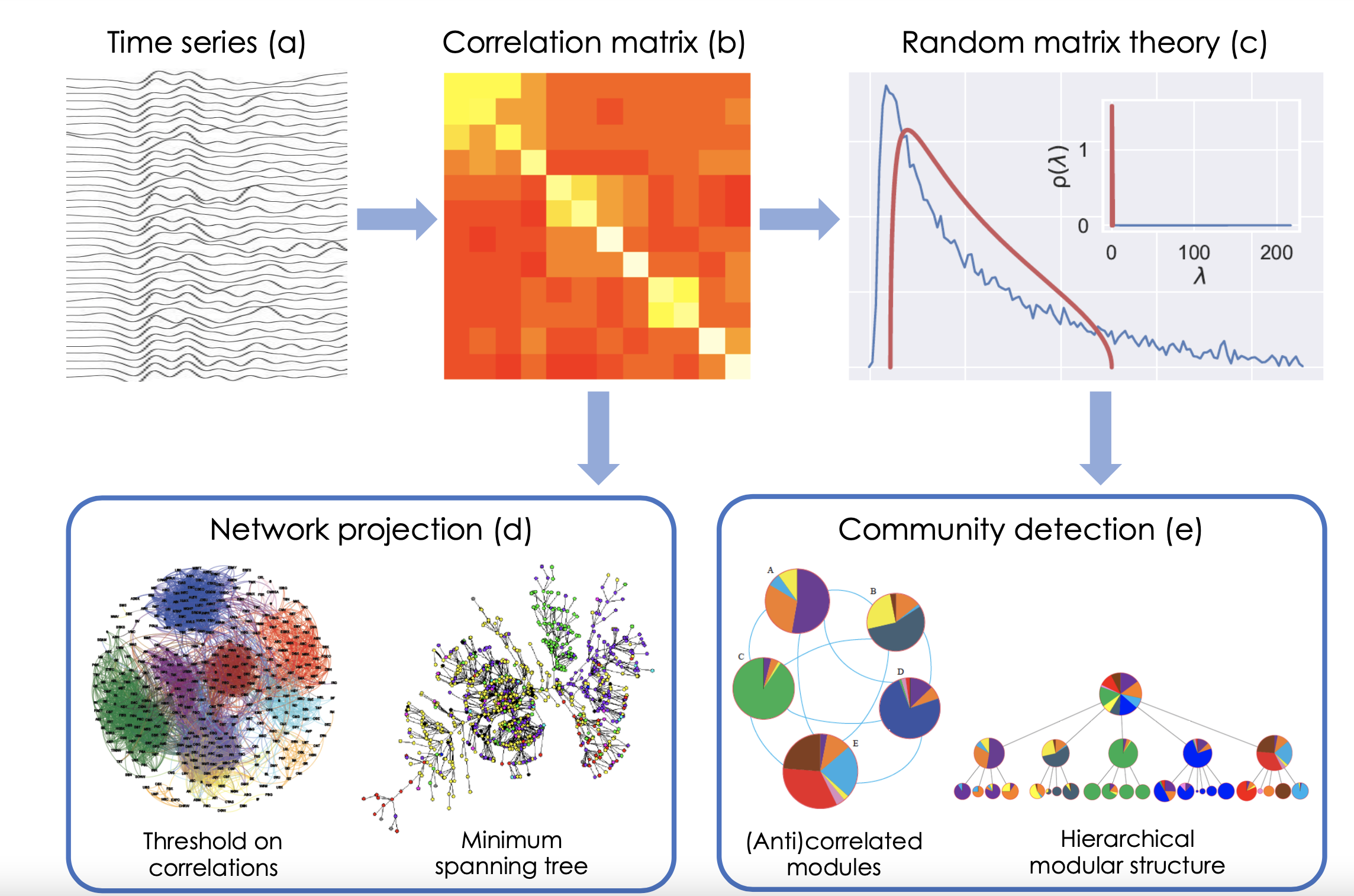

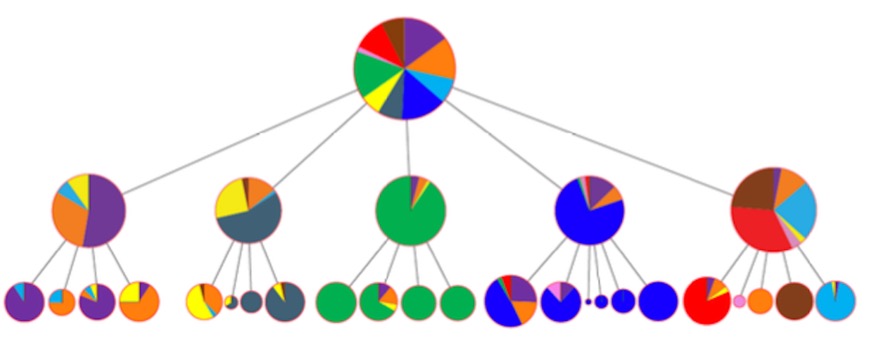

Procedure illustration for the analysis of network structures and their communities out of time series data.

{kind=link}